Weighted Average Cost of Capital (WACC)

Weighted Average Cost of Capital (WACC)

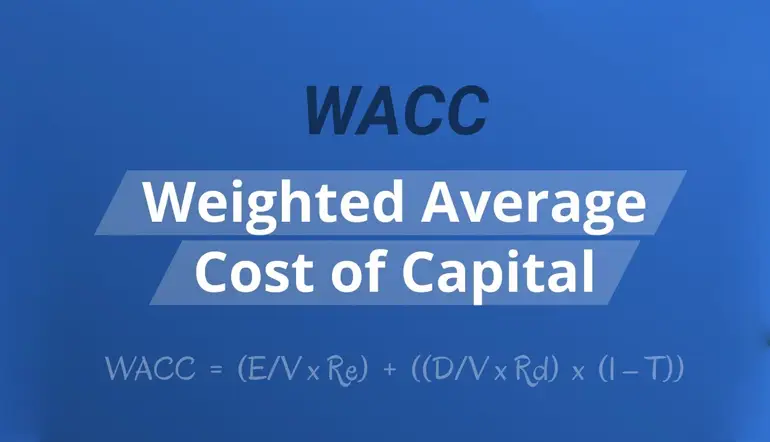

The Weighted Average Cost of Capital (WACC) is the average cost to a corporation of the capital invested in the company's assets. This is made up of a possible mix of debt, preferred stock, common stock, and retained earnings. The current market rates are used to calculate all components of the cost of capital.

What is the WACC Weighted Average Cost of Capital?

WACC (Weighted Average Cost of Capital) is the average cost to a corporation of the funds invested in the company's assets. This is made up of a possible mix of debt, preferred stock, common stock, and retained earnings. The current market rates are used to calculate all components of the cost of capital.

When a company needs money to buy assets, it can get it from a variety of places. Investors will purchase equity shares in the firm, investors will purchase bonds issued by the company, and the company will be able to keep the earnings generated by its activities. Capital projects can be funded using any combination of these sources. There is a cost to acquire any of these funds, equity owners expect a return on their investment, and bond holders expect a regular interest payment.

If a person borrows money, they are required to pay interest on that money. If the individual then invests these funds, the investment return should be greater than the interest cost of the borrowed cash.

This is the same idea that applies to a company's WACC (Weighted Average Cost of Capital). A company is supposed to make capital-allocation decisions that benefit its shareholders. If the company is unable to undertake a capital investment that will boost shareholder returns, the money should be distributed directly to shareholders as a dividend.

The WACC (Weighted Average Cost of Capital) becomes the capital project's hurdle rate. A capital project is initiated when a company purchases assets with the goal of generating revenue that exceeds the cost of capital. To examine if the project will benefit shareholders, cash flow measures will be employed. Annual cash flows are predicted and discounted using the WACC Weighted Average Cost of Capital rate. If the net present value is positive, the project will generate enough profit to cover the cost of capital plus a surplus return.

This is a critical notion to grasp. Because a firm's cost of capital is weighted by the amount of each component, changes in the size of any component might affect the WACC Weighted Average Cost of Capital. This, in turn, can alter how a company behaves. Projects that were previously rejected may now be authorized if the WACC Weighted Average Cost of Capital is reduced.

It is critical to understand this because each new project undertaken by a firm is frequently funded from a single source. If a company's capital structure is 30% debt and 70% equity, it is improbable that new initiatives will be funded in the same proportions. Furthermore, the profit from prior projects that is spent in new capital projects by the corporation might modify the capital structure weighting. If a company consistently uses retained earnings to fund new capital projects, the equity weighting will rise as the size of retained earnings grows relative to the size of debt. Because the cost of equity is frequently higher than the cost of debt, the overall WACC Weighted Average Cost of Capital will tend to rise over time. This could hinder a company's future growth if it is unable to find new capital projects that will cover the higher WACC Weighted Average Cost of Capital rate.

How do you compute the WACC (Weighted Average Cost of Capital)?

We now need to learn how to calculate the WACC Weighted Average Cost of Capital, now that we know what the WACC Weighted Average Cost of Capital is. To accomplish this, we compute the cost of each component of the WACC Weighted Average Cost of Capital and then weigh each cost in relation to its position in the capital structure.

There are two major phases to calculating WACC Weighted Average Cost of Capital. First, we must determine the price of each component. Capital can be obtained from four different sources. Debt is borrowed from banks, insurance companies, governments, and investors through the issuance of bonds. The interest rate paid to the source of these funds determines the cost of debt.

Preferred shares are related to debt in that preferred share owners get a regular set payment, equivalent to an interest payment. In contrast to debt, preferred shares are never repaid, the shares stay outstanding indefinitely, and dividend payments are made for the duration of the shares' existence.

When a company sells shares to the public, it acquires common equity. Shareholders expect to be compensated for both the usage of their cash and the risk they assume by investing directly in the company as an owner.

A company's retained earnings are derived from the profits generated by its operations. The retained earnings are assumed to be shareholder equity that has been reinvested in the company rather than paid out in dividends.

We must establish the cost of each component, as well as the acquisition expenses, and then adjust these costs for the tax consequences of each financing source. Before determining the cost of each, an important question must be answered.

WACC (Weighted Average Capital Cost) Formula

The WACC calculation (Weighted Average Cost of Capital) is complicated and can be broken down into multiple components. Individual component costs are listed in the sections that follow.

WACC (Weighted Average Capital Cost) Variables

- V=Firm Total Value (Debt + Preferred Shares + Common Equity + Retained Earnings)

- Md=Market Value of Debt

- Mp=Market Value of Preferred Shares

- Mc=Market Value of Common Equity

- Mr=Market Value of Retained Earnings

- K=Current Market Interest Rate

- T=Tax Rate

- DP=Annual Dividends for Preferred Shares

- Pp=Market Price of Preferred Shares

- Fp=Floatation Costs of Preferred Shares

- Dc=Annual Dividends for Common Shares

- Pc=Market Price of Common Shares

- Fc=Floatation Costs of Common Shares

- G=Constant Growth Rate of Common Share Dividends

Debt Cost Calculator

The cost of debt is the expense to the corporation of borrowing capital to finance operations.

K denotes the current market interest rate.

T stands for Tax Rate.

Cost of Preferred Shares Formula

The cost to the corporation of using funds obtained by selling preferred shares to investors is referred to as the cost of preferred shares.

D stands for Annual Dividends.

P = Shares' Market Price

F = Floatation Fees

Cost of Common Shares Formula

The expense to the corporation of issuing common shares to investors is referred to as the cost of common shares.

D stands for Annual Dividends.

P = Shares' Market Price

F = Floatation Fees

G = Dividend Growth Rate Constant

Cost of Retained Earnings Formula

The cost to the corporation of using funds retained from earlier gains is known as the cost of retained earnings.

D stands for Annual Dividends.

P = Common Shares Market Price

G = Dividend Growth Rate Constant